A funny thing happened on the way to the AI market. After months of research for TM Forum a division between telcos who are building data centers for AI and those who are not became clear. And being a BSS market analyst, I wanted to know which BSS providers are winning most among telcos who are building AI data centers. Pretty soon, Power Rankings emerged and I share them below. But here’s how we get there…

Telco AI data centers: Shedders versus Builders

Worldwide, but especially in North America and Western Europe, many telcos have delayered or sold off assets to pay down debt. They have shed data centers, cell towers, and optical fiber to focus on networks and customer experiences with an asset-light telco model. Verizon and AT&T both exemplify this trend and neither is in the AI data center-building business, nor are their regional telco peers.

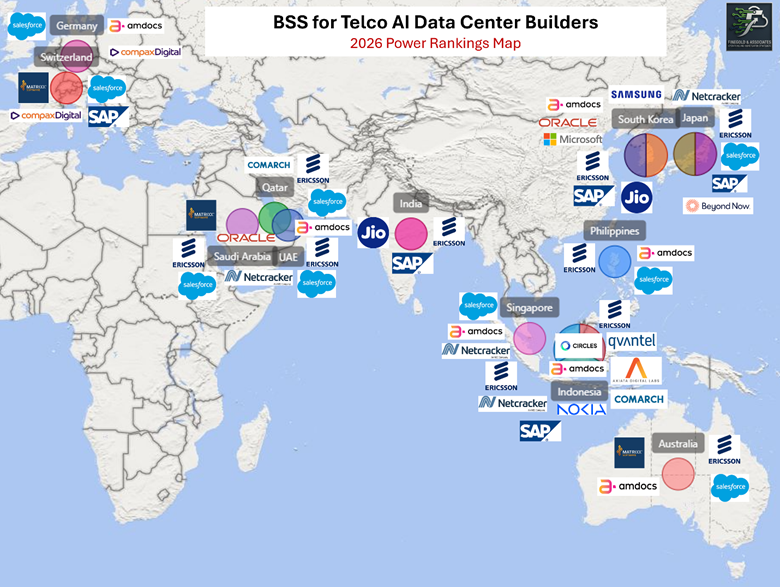

In parts of Europe, like Germany and Switzerland, but especially in markets across Asia and the Middle East, groups of telcos are very much engaged in building AI data centers and are partnered with firms like Nvidia and KKR for capital resources. The map below shows where Finegold & Associates has tracked data center builds by 16 different telcos ranging from Deutsche Telekom, Swisscom, Saudi Telecom and Ooredoo, to PLDT, XL Axiata, Softbank, NTT, Jio, Telstra and more.

Source: Finegold & Associates

Telco BSS for AI data center builders

The next question I aimed to answer was who are the big BSS vendors for these 16 telcos that are actively building AI data centers. There could be dozens of one-off players in the mix, but I wanted to see if the big BSS vendors are engaged in this capital-rich market sub-segment. The underlying assumptions is, if you win in this segment, you are winning in one of the few exciting growth sectors telecom has to offer, and that is good for your BSS business.

I added the BSS vendors to the map of data center builders:

Source: Finegold & Associates

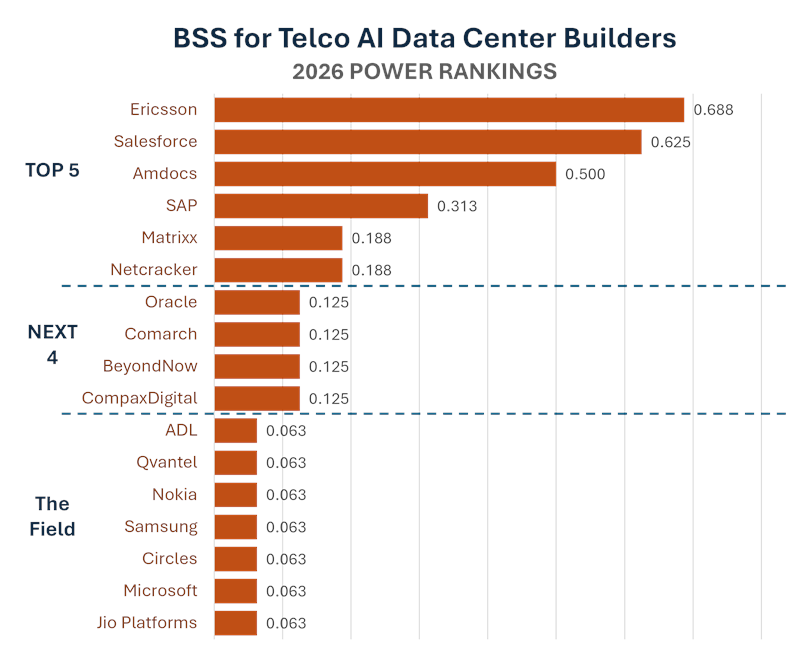

We put all this data in a table, which we will keep in-house for now, and quantified the market at a high level. We looked at the total number of telcos tracked, 16 in this case, and noted which vendors provide them with BSS ranging from billing and rating to charging and CRM. We then calculated the percentage of this telco sub-segment with which each BSS vendor is engaged, as far as we can determine based on public data. We then organized rankings based on highest to lowest percentage of engagement with the market to produce our Power Rankings.

BSS for Telco AI Data Center Builders: 2026 Power Rankings

And here are the rankings:

#1: Ericsson (.688)

Coming in at number one in our rankings is Ericsson Software, which provides monetization and charging technology and services for leaders across APAC and the Middle East like Softbank, Telkom Indonesia, Ooredoo, and Saudi Telecom. Ericsson serves nearly two-thirds of the telco data center builder market segment with BSS. Ericsson’s dominance of the telco equipment market has certainly helped here.

#2: Salesforce (.625)

Salesforce is deeply embedded as a primary CRM platform across telco markets. It is installed in the data center builder sub-segment with leaders like Singtel, Softbank, Ooredoo, and Saudi Telecom as well as with Deutsche Telekom. As a deep-pocketed, AI-savvy company itself with deep experience in telco, Salesforce makes sense as a partner for AI data center building telcos.

#3: Amdocs (.500)

Watch out for Amdocs! By acquiring 5th ranked MATRIXX Software, Amdocs should soon overtake Ericsson for the top spot in these power rankings. We decided to treat Matrixx as a separate entity in this edition because the acquisition has been announced, not completed. This gives a view of how this acquisition will expand Amdocs’ global position and strength among telcos that are building AI data centers. Key accounts include e&, PLDT, Singtel, and Telkom Indonesia.

#4: SAP (.313)

SAP’s sheer presence across key geographies like Germany, Switzerland, Indonesia, Japan and South Korea, where data center building is active among telcos, gives it a leg up as the other major CRM provider, as well as in BSS data management.

#5: Matrixx Software (.188)

Matrixx Software, soon to be part of Amdocs, brings some key real estate to the Amdocs footprint in the data center builder market. Its relationships with Telstra in Australia, Saudi Telecom in Saudi Arabia, and Swisscom in Switzerland, for example, further bolster Amdocs presence in these accounts and geographies.

#5: Netcracker (.188)

Tied for fifth with Matrixx, Netcracker Technology’s presence as a BSS provider in this market sub-segment is relatively limited given it is otherwise one of the two biggest BSS providers in the industry. Its position as an OSS provider, taken separately, is more dominant. Relationships with key accounts like Singtel and Softbank for BSS, however, put Netcracker at the center of the action as these telcos build out AI data centers with capital partners like KKR, Nvidia, and Softbank.

Watch Qvantel, BeyondNow

Much like the greater BSS market, we have participants in this sub-segment ranging from giants like Oracle and Microsoft to specialists like Comarch and CompaxDigital. Within their key accounts, these vendors all play critical monetization or customer experience roles, just not in a discernible pattern across this entire space.

Though Qvantel did not rank highly in these power rankings, we can recognize its upward momentum, having recently acquired Optiva. Qvantel is also the primary monetization provider for XL Axiata which serves nearly 60 million subscribers in Indonesia and is actively building AI data centers with capital partners like Princeton Digital Group. Don’t be surprised to see Qvantel emerge a bit from this pack.

Beyond Now caught my eye in this study because it’s unique approach to partner marketplaces and B2B2x business models has taken root in Japan with Softbank and NTT. This bears watching as the growth of the AI ecosystem and its component-based solutions has not really begun to cook yet. Beyond Now should benefit from more sophistication and partner activity as more data centers, connectivity, and AI resources go online. (For more specifics, this past article provides a close look at Beyond Now.)

The bottom line?

Watch out for Amdocs. This should be your standing advice for participating in the telco BSS business anyway, but in the sub-segment of telcos building AI data centers, Amdocs has the momentum and should soon have the lead.