I remember people marveling when in 2006 Oracle bought Portal Software for about $220 million in cash. It seemed like a big win at the time. Just last week, Portal founder Dave Labuda did it again, this time selling MATRIXX Software to Amdocs for a reported $200 million in cash.

So far, the scuttlebutt says this is a ho-hum deal. But this acquisition makes sense for Amdocs, not just in the charging business, but also in the raging battle against Netcracker in the BSS landscape. That said, its limited value says a lot about the future relevance of telco charging.

Why acquiring Matrixx makes sense for Amdocs

At Finegold & Associates we try to track relationships between major BSS vendors and 100 major telcos around the world. The data we share here is based on publicly accessible information, so we can’t promise it’s perfect, but we have enough data to provide a relevant view.

Source: Public announcements, vendor websites, collated by Finegold & Associates

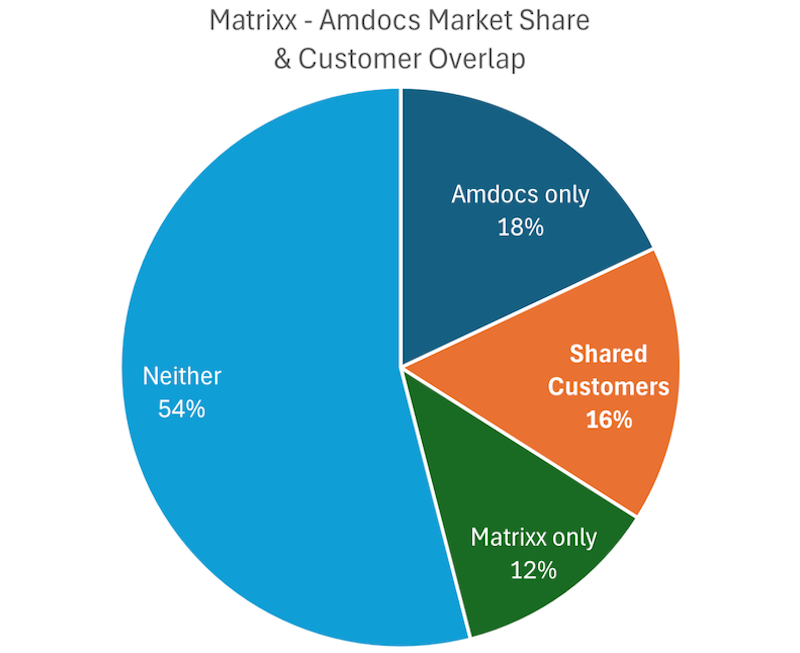

Earlier this week, we shared some data on LinkedIn (see chart) showing the overlap between the Matrixx and Amdocs customer bases prior to the acquisition. It is significant.

Of the 100 telcos we track, we noted 16 instances where a telco was a customer of both Amdocs and Matrixx. This is 35% of the total customer base of the joined-up companies, 47% of the Amdocs customers we have tracked, and 57% of Matrixx’ customers.

With that much shared customer landscape, an acquisition of Matrixx by Amdocs seemed inevitable.

It makes sense for Amdocs to continue to expand its charging business. This move is additive to its $180 million acquisition of Openet from 2020. It gives Amdocs footholds in 12 new accounts. It makes Amdocs the only telco charging provider not owned by a telecom equipment maker. And it gives Amdocs some inorganic revenue growth in a category that isn’t organically growing.

How acquiring Matrixx fends off Netcracker

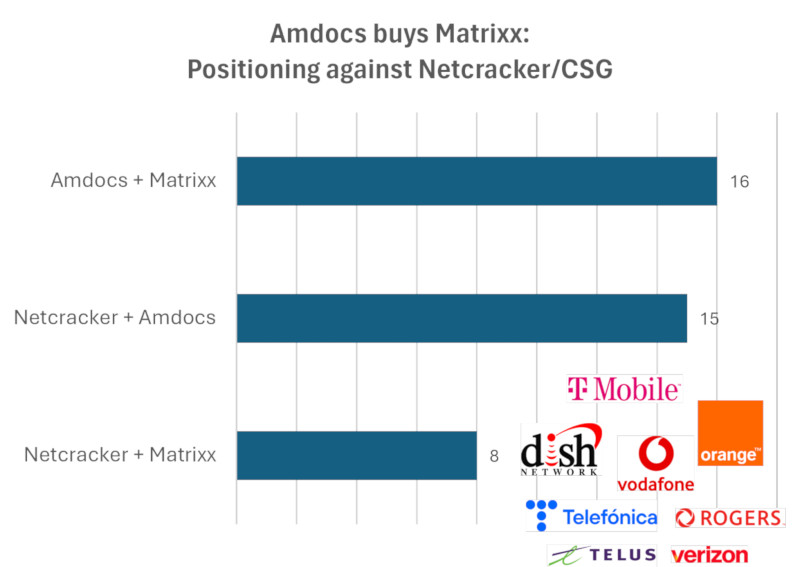

Amdocs acquisition of Matrixx also helps defend a bunch of key accounts against Netcracker. While digging into Amdocs and Matrixx shared accounts, we cross-checked our Netcracker data and stumbled on some interesting factoids (see chart).

- There are 16 instances of Amdocs and Matrixx sharing clients prior to the acquisition.

- There are also 15 instances where Amdocs and Netcracker share accounts, sometimes on an OSS versus BSS basis, sometimes fixed line versus mobile, or retail versus wholesale BSS for example, depending on the account.

- There are no instances where Netcracker and Matrixx share a customer without Amdocs also having previously had a presence within the account.

- There are 8 instances where Netcracker, Amdocs, and Matrixx all inhabit the account. And they are significant.

As the chart shows, Amdocs acquisition of Matrixx can serve as a check against Netcracker, particularly in the mobility business across a range of major, shared customers. This group of high value, shared accounts where all three vendors already operate includes Dish Network, Orange, Rogers, T‑Mobile US, Telefonica, Telus, Verizon, and Vodafone. The battle for primacy in these types of accounts has only intensified between Amdocs and Netcracker since the latter’s parent, NEC, announced in October 2025 it would acquire CSG International. By acquiring Matrixx, Amdocs gains some added ground across 8 contested accounts.

Why this deal shows telco charging is becoming irrelevant

As an industry we might like to talk about how much revenue and economic opportunity charging has enabled thanks to the growth of mobility.

Yet the cloud and AI industries haven’t adopted telco charging standards or technologies from Amdocs, Netcracker, Matrixx, Ericsson, Nokia et al. by and large, to create their real-time, observable metering platforms and build billions, if not trillions, in business value. That’s a whole load of value in measuring and charging for tech usage that did not require standardized telecom charging to evolve.

A hidden back story of the Matrixx acquisition is that the charging business is a sideshow.

Charging is rigorously standards-based and then changes dramatically from one mobile generation to the next. Mobile standards creation is a slow process that tries, and often fails, to predict future market needs. It provides an opportunity for vendors to put their thumbs on the scales within the standards making process. And it’s out of sync with most or all other tech trends around it.

Game changers like AI, APIs, and cloud applications have benefitted from mobility. Regardless, standardized mobile network charging is not high on the list of key enablers for these global scale technology phenomena.

Which begs the question — what does it say that Matrixx is being acquired by Amdocs for about the same value that Oracle acquired Portal 20 years ago? It shows that telco-specific, standards-based charging has limited value going forward. It will continue to play roles within the mobile network domain but charging has proven to be neither an enabler nor a rate limiter for the massive growth of parallel markets like cloud services and AI.